Withdrawing money in Thailand can cost more than many travellers expect. For years, most guides mentioned ATM fees of around 220 baht. But in 2026, some ATMs now display higher fees, including 250 baht with Visa and up to 350 baht with some foreign Mastercard cards.

On top of these local ATM fees, your own bank may charge extra withdrawal fees, apply a poor exchange rate or offer dynamic currency conversion. Here is what you should check before withdrawing Thai baht in Thailand.

Key things to know before withdrawing money in Thailand

- ATM fees in Thailand are no longer always 220 baht.

- Some Thai banks now charge 250 baht with Visa and up to 350 baht with Mastercard.

- With a foreign card, always check the fee displayed on the ATM screen before confirming.

- If the ATM offers to convert the amount into euros, dollars or pounds, choose to be charged in Thai baht instead.

- To reduce the impact of fixed ATM fees, avoid making several small withdrawals.

Last updated: June 2026. Fees may vary depending on the Thai bank, card network, card type and the terms of your own bank.

How Much Do ATM Fees Cost in 2026?

In Thailand, ATMs usually charge a fixed fee when you withdraw money with a foreign card. This fee is charged by the Thai bank that owns the ATM, separately from any fees that may be charged by your own bank.

Many articles still mention a withdrawal fee of around 220 baht. This figure may still appear in older guides or outdated content, but it no longer always reflects what travellers may see in 2026. Several Thai banks now display fees of 250 baht, and sometimes 350 baht, depending on the card network used.

Scroll horizontally on mobile if needed.

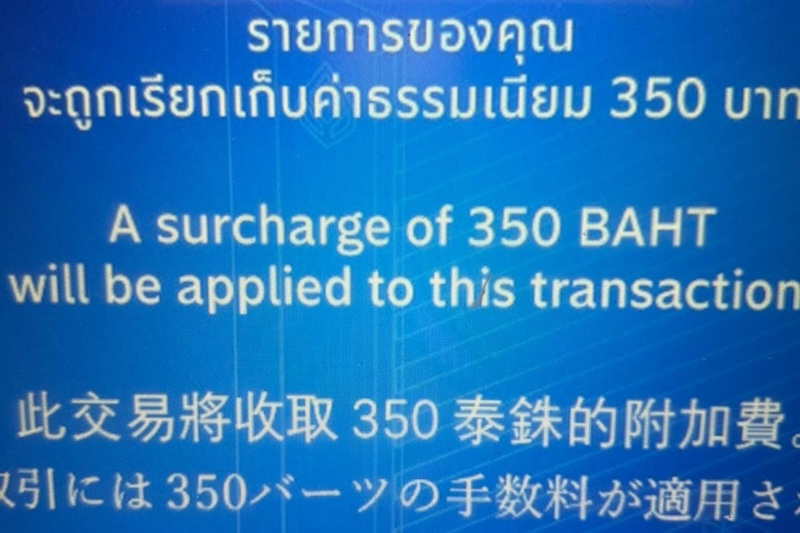

Mastercard 350 Baht: Is This Really the New ATM Fee?

You should not assume that every ATM in Thailand now charges 350 baht. That would be too broad. However, it is clear that 350 baht ATM fees do exist, especially for some withdrawals made with a foreign Mastercard card.

During our latest test in Thailand, we tried three different ATMs with a foreign Mastercard card. In all three cases, the fee displayed before confirming the transaction was 350 baht. This does not mean that every ATM will always apply this fee, but it confirms that 350 baht fees can now apply to some Mastercard withdrawals in Thailand.

On-the-ground observation

With a foreign Mastercard card, several ATMs tested in Thailand displayed a fixed 350 baht fee before confirmation. Before validating a withdrawal, always read the screen carefully. If the fee seems too high, cancel the transaction and try another ATM or another card.

This change matters because many travellers still arrive in Thailand expecting ATM withdrawals to cost around 220 baht. In 2026, it is safer to expect a range of 250 to 350 baht, depending on the ATM and the type of card used.

Which Thai Banks Display 250 or 350 Baht ATM Fees?

Available information does not make it possible to say that all Thai banks apply exactly the same fees. However, some official fee schedules clearly show a difference between Visa and Mastercard withdrawals.

To be safe, do not assume that all ATMs cost the same. The best habit is to check the fee displayed before confirming the withdrawal. If you have two cards, for example a Visa and a Mastercard, it may be worth comparing the fees shown by the ATM.

You can check the official fee schedules from Krungsri and Kasikorn Bank to verify the fees displayed by these banks.

Can You Avoid ATM Fees by Withdrawing Money at a Bank Counter?

Some travellers recommend withdrawing money directly inside a bank branch, at the counter, with your passport. This method may sometimes work depending on the bank, branch and card used, but it should not be presented as a guaranteed solution.

At Krungsri, for example, the official fee schedule indicates a 200 baht fee for some over-the-counter withdrawals with an international Visa card. This may be cheaper than some ATM withdrawals, but it is not free.

Be careful with bank counter withdrawals

Withdrawing money at a bank counter may sometimes avoid certain ATM fees, but it is not guaranteed. The bank may refuse, apply its own fees, ask for your passport or process the transaction as a cash advance depending on your card type. Also check the fees charged by your own bank before using this method.

If you use a credit card, be especially careful. A withdrawal at a bank counter or ATM may be treated as a cash advance, with additional fees and sometimes immediate interest. With a debit card, the risk is usually lower, but the conditions always depend on your bank.

DCC: Should You Accept the ATM’s Currency Conversion?

No, in most cases, it is better to refuse the currency conversion offered by the ATM and choose to be charged in Thai baht.

When withdrawing money in Thailand, the ATM may offer two options:

- to be charged in Thai baht;

- to be charged directly in your home currency, such as euros, US dollars, Swiss francs or British pounds.

The second option may look reassuring because you immediately see the amount in your own currency. But this is often where dynamic currency conversion, also called DCC, comes in. In that case, the ATM or payment operator applies its own exchange rate, often less favourable than your card’s rate.

The right choice at the ATM

- If the ATM asks: “Convert to EUR / USD / GBP?” → refuse the conversion.

- If the ATM asks which currency you want to be charged in → choose THB / Thai Baht.

- Let your bank, Wise, Revolut, N26 or card provider handle the conversion.

To avoid marked-up exchange rates linked to dynamic currency conversion, generally choose the local currency, meaning Thai baht, rather than a converted amount in your home currency.

Should You Withdraw in Baht or in Your Home Currency?

You should withdraw in Thai baht. It is the local currency, and it is usually the most transparent option.

If the ATM shows you an amount in euros or another currency, that does not necessarily mean you are saving money. On the contrary, this option may include an unfavourable exchange rate. The displayed amount may look convenient, but it is often more expensive than letting your bank or card provider handle the conversion.

How Much Should You Withdraw Each Time?

Since ATM fees are fixed, small withdrawals are the least cost-effective. Whether you withdraw 3,000 baht or 20,000 baht, the ATM fee may be the same. The lower the amount withdrawn, the higher the fee is as a percentage of your withdrawal.

In practice, it is often better to withdraw a larger amount and then keep the cash safely at your accommodation. However, avoid walking around with too much cash on you, especially in very touristy areas or during transfers.

What Is the Maximum Amount You Can Withdraw in Thailand?

The maximum amount depends on two limits:

- the limit set by the Thai ATM;

- the limit set by your own card or bank.

Many Thai ATMs allow withdrawals of between 20,000 and 30,000 baht per transaction, but this can vary depending on the bank and the machine. Some ATMs offer less, while others may allow more. Your own bank may also block the withdrawal if your daily or weekly limit is too low.

Before travelling, check:

- your overseas withdrawal limit;

- your card payment limit;

- your foreign transaction fees;

- whether you can temporarily increase your limits through your banking app.

Wise, Revolut, N26: Are They Really Fee-Free in Thailand?

Cards such as Wise, Revolut or N26 can be useful when travelling, as they often help reduce currency exchange fees or foreign payment fees. But you need to separate two different types of fees:

- fees charged by your own bank or banking app;

- fees charged by the Thai bank that owns the ATM.

Even if your bank or neobank does not charge withdrawal fees within certain limits, the Thai ATM may still apply its own local fee. That is why a withdrawal can cost 250 or 350 baht even with a travel-friendly card.

To better understand the guarantees and limits of cards while travelling, you can read our guide to credit card travel protection.

The ideal approach is to have at least two payment methods: a main card, a backup card and some cash. In Thailand, card payments are common in hotels, shopping malls and modern restaurants, but cash remains very useful for markets, small restaurants, taxis, tuk-tuks, scooters, excursions and everyday expenses.

Should You Bring Cash or Withdraw Money in Thailand?

Both options can make sense. Withdrawing money in Thailand is convenient, but fixed ATM fees can become expensive if you make several small withdrawals. Bringing some cash and exchanging it locally may be useful, especially if you use a good exchange booth and your banknotes are in good condition.

However, you should not carry your entire travel budget in cash. A balanced approach usually works best:

- some cash to exchange locally;

- a main bank card;

- a second backup card;

- only a few ATM withdrawals, while avoiding repeated small withdrawals.

Cash or Card: What Should You Use in Thailand?

Thailand is still a country where cash is very useful. In tourist areas, you can often pay by card in hotels, shopping malls, some restaurants, modern shops or tour agencies. But for many everyday expenses, cash remains essential.

How to Reduce ATM Withdrawal Fees in Thailand

It is difficult to completely avoid ATM fees in Thailand, but you can reduce them with a few simple habits.

Best practices

- Withdraw less often, but take out larger amounts.

- Avoid withdrawing 2,000 or 3,000 baht several times.

- Refuse dynamic currency conversion and choose to be charged in baht.

- Try a Visa card if your Mastercard displays a 350 baht fee.

- Always keep a second card as a backup.

- Check your withdrawal limits before travelling.

- Compare the fees displayed by different ATMs before confirming.

If you stay several weeks in Thailand, these differences can become significant. Three withdrawals at 350 baht already represent 1,050 baht in ATM fees, not including any additional fees charged by your own bank.

Common Mistakes to Avoid

Here are the most common mistakes travellers make when withdrawing money in Thailand:

- Accepting the conversion in euros or another currency offered by the ATM.

- Withdrawing small amounts too often.

- Assuming Wise, Revolut or N26 removes all fees, including Thai ATM fees.

- Not reading the screen before confirming, especially if the displayed fee is 350 baht.

- Travelling with only one card.

- Forgetting your withdrawal limits.

- Confusing ATM fees, exchange fees and bank fees.

Should You Avoid ATMs at the Airport?

ATMs at the airport are convenient, especially if you arrive without Thai baht. ATM fees are usually displayed before confirmation, just like elsewhere. The main issue is the lack of choice, and the fact that travellers are often tired, rushed or less attentive after a long flight.

If you need to withdraw money at the airport, take out a reasonable amount for your first expenses: taxi, transport, food, eSIM or small emergencies. You can then compare ATMs or exchange booths more calmly in the city.

What Strategy Should You Use Before Travelling?

Before your trip, a simple strategy can help you avoid stress:

- bring both a Visa card and a Mastercard if possible;

- carry some cash to exchange locally;

- check your bank’s foreign withdrawal fees;

- temporarily increase your limits if needed;

- save your bank’s emergency number;

- avoid keeping all your cards and cash in the same place.

This simple preparation can save you a lot of stress once you arrive. For a broader overview, you can also read our Thailand travel checklist.

FAQ About ATM Withdrawals in Thailand

Are ATM fees in Thailand always 220 baht?

No. Many guides still mention 220 baht, but in 2026 some ATMs display 250 baht, or even 350 baht with certain foreign Mastercard cards.

Why does my Mastercard show a 350 baht ATM fee?

Some Thai banks now charge higher fees for withdrawals made with foreign Mastercard cards. At Krungsri and Kasikorn Bank, recent fee schedules show 350 baht for Mastercard, compared with 250 baht for Visa or UnionPay.

Is Visa cheaper than Mastercard at Thai ATMs?

In some banks, yes. Official fee schedules show 250 baht for Visa and 350 baht for Mastercard. This is not necessarily the case everywhere, so always check the fee displayed on the ATM screen before confirming.

Should I choose euros or baht at the ATM?

Choose Thai baht. If you choose to be charged in euros or another currency, the ATM may apply dynamic currency conversion with an unfavourable exchange rate.

Can I avoid ATM fees by withdrawing at a bank counter?

Not always. Some banks may charge a fee at the counter, refuse the transaction or ask for your passport. At Krungsri, some over-the-counter withdrawals with an international Visa card are charged 200 baht. This method should not be presented as a guaranteed way to avoid fees.

How much should I withdraw each time?

Since the fee is fixed, it is better to avoid repeated small withdrawals. Withdrawing 10,000, 20,000 or 30,000 baht may be more cost-effective than withdrawing 2,000 or 3,000 baht several times, as long as you keep the money safe.

Can Revolut, Wise or N26 avoid Thai ATM fees?

These cards can reduce the fees charged on your side, but they do not necessarily remove the fees charged by the Thai ATM. If the ATM displays a 250 or 350 baht fee, that fee may apply even with a travel card.

What Should You Check Before Confirming an ATM Withdrawal in Thailand?

Withdrawing money in Thailand is still simple, but fees have become more variable than before. In 2026, you should no longer rely only on the old figure of 220 baht. Some banks now display 250 baht with Visa and up to 350 baht with Mastercard.

The key rule is to read the ATM screen carefully before confirming, refuse dynamic currency conversion, choose Thai baht and avoid repeated small withdrawals. If you have several cards, test the one that displays the lowest fee. Over a stay of several weeks, these choices can save you a meaningful amount of money.